Financial Disclaimer: The strategic analysis from the Finanlytic Data Intelligence Unit is meant for informational and educational purposes only. Content created by Hugo Cutillas or other contributors shouldn’t be taken as professional investment, financial, tax, or legal advice. Trading in fast-paced markets carries a significant risk of losing capital. Finanlytic is not a registered financial advisor or broker-dealer. We analyze complex data signals, but remember, just because something worked in the past doesn’t guarantee it will work in the future. Always do your own research and consult with a certified financial professional before making any market moves.

The concept of the “Middle Class” has shifted dramatically; by 2026, it’s morphed into what we now call a liquidity trap. We’re seeing a significant separation of labor from wealth. While salaries for professionals still rise in line with inflation, the costs of essential assets, like real estate, energy, and stocks, are skyrocketing at an exponential rate.

At the Finanlytic Intelligence Unit, we refer to this phenomenon as Asset Poverty: a situation where even high earners find themselves in a precarious position because they lack ownership of valuable assets that generate income while they sleep.

The Maintenance Mode Trap

For many years, the middle class thrived on a Growth Model. But nowadays, that’s shifted to what we call Maintenance Mode. By 2026, the “Cost of Existence” has turned into an unavoidable tax on our professional lives. When a staggering 60% of a household’s post-tax income goes towards housing, private healthcare, and the “Energy Friction” we’ve discussed before, individuals find themselves not building wealth but simply paying for the privilege of staying in the workforce.

The mental burden of 2026 isn’t just about soaring prices; it’s about Structural Fragility. Earning a six-figure salary no longer guarantees a secure life; instead, it feels more like a pricey subscription to a lifestyle that can be abruptly canceled by a single corporate shake-up or an algorithm shift.

DATA INTELLIGENCE UNIT

| Metric | The 1990s Social Contract | The 2026 Structural Reality | Finanlytic Impact |

| Primary Wealth Driver | Career Progression | Asset Appreciation | Labor value is collapsing vs. Capital. |

| Housing Multiplier | 3x Annual Salary | 8x – 14x Annual Salary | The “Starter Home” is a dead concept. |

| Financial State | Accumulation & Growth | Survival & Maintenance | Savings are eroded by non-discretionary costs. |

| Economic Identity | Professional / Worker | Investor / Asset Owner | If you don’t own the machinery, you are the fuel. |

The Salary Ceiling and Cognitive Task Erosion

The “Middle Class Squeeze” is getting worse, thanks to the Wage Compression we’ve highlighted in our AI reports. By 2026, the value of simply “doing” has taken a nosedive. Those mid-level management and administrative jobs, which used to be the backbone of middle-class stability, are now being eroded.

With a “Super-Employee” capable of handling the workload of three people thanks to AI, corporate leaders have capped salaries. We refer to this as The Efficiency Tax: you might be 300% more productive, but your purchasing power has actually dropped by 0.5% when you factor in the soaring costs of essential goods that you can’t avoid.

The Psychological Toll

Predictability used to be the go-to product for the middle class. Fast forward to 2026, and it’s become a luxury. The unsettling reality that a decade’s worth of careful saving can vanish in an instant due to a “Black Swan” event, whether it’s a health crisis, a geopolitical shake-up, or a tech disruption, has led to a pervasive state of Chronic Economic Anxiety. This sense of vulnerability pushes professionals into a defensive position, putting off starting families and stifling the very creative risk-taking that once drove our economy forward.

The Finanlytic Playbook: Moving from Labor to Equity

The age of the “Good Employee” has come to an end. To navigate the challenges of 2026, we need to shift our focus from simply maximizing income to acquiring assets.

Let go of Loyalty and Embrace Mobility: In a time when wages are stagnating, the most significant pay increases often come from changing jobs or exploring “Side-Equity” opportunities.

Prioritize Judgment over Execution: As AI takes over routine tasks, the ability to make high-context decisions becomes increasingly valuable. It’s about selling your ability to say “Yes” or “No,” rather than just how to get things done.

Strategic Asset Positioning: Every dollar you earn should be seen as a soldier sent out to seize a part of the “Fortress.” Whether it’s investing in fractional real estate through tokenization or acquiring equity in automated systems, ownership is the key to breaking free from Maintenance Mode.

To visualize the structural shift of 2026, we must look at the widening gap between productivity and median compensation. While asset prices have decoupled from labor value, the “squeeze” has become a measurable global phenomenon.

(Note: This data confirms that while the middle class remains the demographic core, its share of aggregate income has shifted toward the ‘Fortress Class’ of asset owners.)

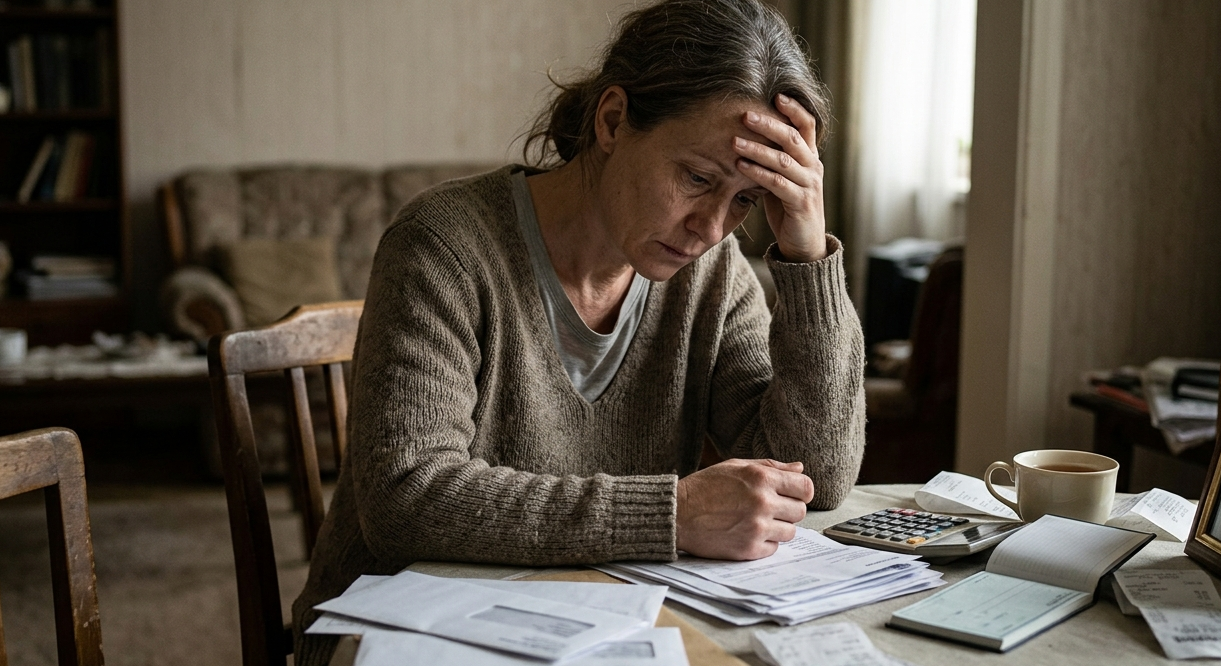

The middle class was originally built on a foundation of predictability. When that predictability is removed, it is replaced by chronic anxiety. Even households with six-figure incomes now report feeling “economically fragile.” The pervasive sense that a single medical incident or a corporate “restructuring” could wipe out a decade of progress is a constant mental drain. This fragility fundamentally changes societal behavior: people take fewer creative risks, they delay starting families, and they become increasingly cynical about the future. This shift from “Growth Mode” to “Survival Mode” is the defining psychological challenge of our time.

Finanlytic Takeaway

FINANLYTIC | DATA INTELLIGENCE UNIT | Analysis by Hugo | Lead Market Strategist

The “Middle Class Dream” isn’t just fading away because of a recession; it’s actually being replaced by a whole new system. By 2026, thinking you’re “comfortable” could be a risky misconception that masks your lack of power. This system is set up to squeeze every bit of effort from you while charging you top dollar just to exist. To really succeed, you need to shift your mindset from being just a worker to becoming an Architect of Assets.

The tools for this Great Rewiring, like tokenization, leveraging AI, and embracing global mobility, are at your fingertips, but they demand a commitment to stop getting caught up in the numbers and start focusing on your position. If you don’t have a stake in the economy of 2026, you’re merely a resource being managed by it.